Difference Between IBAN Bank Codes and SWIFT Codes

A routing number is a nine-digit numeric code printed on the bottom of checks to facilitate the electronic routing of funds (ACH transfer) from one bank account to another. It's also referred to as an RTN, a routing transit number, or an ABA routing number. You can use your routing number and account number supplied by your bank to help facilitate the processing of electronic transfers. It is the same number you would use for Direct Deposit or if you use online bill pay.

There are only two internally recognized and standardized ways of identifying a bank account when doing any transaction from one country to the other, namely the IBAN Bank codes and the SWIFT codes. Here is what you need to know about routing numbers.

The difference between IBAN Bank codes and SWIFT codes

Your account number (usually 10-12 digits) is specific to your account. It's the second set of numbers printed on the bottom of your checks, just to the right of the bank routing number. You can also find your account number on your monthly statement. IBAN Bank Code: The IBAN consists of an alphabetical country code, followed by two digits, and then up to thirty-five characters for the bank account number. While the BBAN (Basic Bank Account Number) will contain the country-specific details of your bank account number, the IBAN will have both your country-specific details and information that identifies the country in which your bank account is held.

IBAN Bank Codes

The International Bank Account Number (IBAN) is an internationally agreed system of identifying bank accounts across national borders to facilitate the communication and processing of cross-border transactions with a reduced risk of transcription errors. It was initially adopted by the European Committee for Banking Standards (ECBS) and was later adopted as ISO 13616:1997 standard in 1997, and now as ISO 13616:2007.

IBAN stands for International Bank Account Number and is attached to all accounts in the EU countries plus Norway, Switzerland, Liechtenstein, and Hungary. The IBAN is made up of a code that identifies the country the account belongs to, the account holder's bank, and the account number itself.

Advantages of IBAN Bank Codes

IBAN Bank codes have 2 main advantages. First, they make it easier for banks to process international payments productively. Second, and most importantly, because every country's national bank system already has a unique identity, adding a few more characters onto this mark allows it to create a truly universal identifier that will enable it to quickly and unambiguously identify individual banks with the value of potential errors and transaction times radically reduced.

Disadvantages if IBAN Bank Codes

All banks will have to update their system with the IBAN bank codes, making them modern and secure. So, all bank accounts in the EU will be replaced by IBAN bank accounts, and the IBAN bank codes will replace BIC codes. It is mandatory to use IBAN bank codes for banking transactions both within Europe and between Europeans and people holding accounts in non-European countries. This is because banks are more than just financial institutions; they are also computers, and they need to be able to communicate with each other. They would not be able to do this if they used different formats for database or account numbers or even different registration procedures.

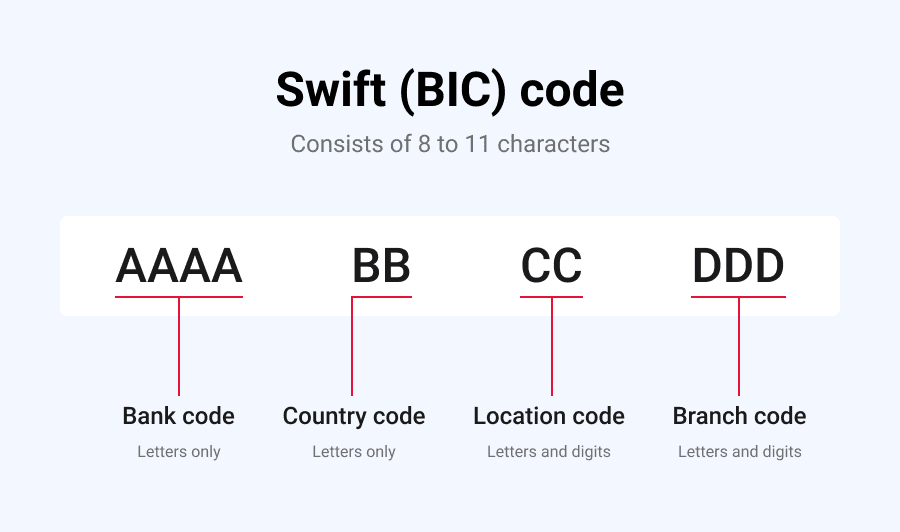

SWIFT Codes

SWIFT Codes help to identify where a bank branch is located. SWIFT stands for Society for Worldwide Interbank Financial Telecommunication, which handles the exchange of most international wire transfers. A SWIFT code is an 8-11 character code that uniquely identifies financial institutions worldwide. These codes are used when transferring money between banks, particularly for international wire transfers. Banks also used the codes for exchanging other messages between them.

While every effort is made to provide accurate data, users must acknowledge that this website accepts no liability whatsoever with respect to its accuracy. Only your bank can confirm the correct bank account information. If you are making an important payment, which is time-critical, we recommend you contact your bank first.

Advantages of SWIFT Codes

Using a SWIFT code is faster and more efficient than using checks. Each SWIFT code corresponds to 1 bank/bank branch worldwide. Banks use SWIFT codes to identify each other when sending or receiving money internationally. Banks use these codes to process international wire transfers and messages.

Disadvantages of SWIFT Codes

Though SWIFT certainly has some advantages, there are also disadvantages to using their codes. The most significant burden is the high costs associated with using the codes. When banks send international wire transfers through the SWIFT network, a fee is charged to the sender and again at the receiving institution. Most banks add on their own surcharges in addition to these fees, resulting in high overall costs for the customer.

Conclusion

These are Standardized systems for identifying bank accounts across national borders. Banks use them, credit card companies, transnational and other financial institutions for international money transfers in a secure way. It is necessary to provide your IBAN Bank Code / SWIFT code when sending money abroad. It is also necessary when you receive payments from abroad.

These routing numbers are significant when doing both international and national transactions. Although their charges may still be very high, their contribution to the swiftness of transactions in the countries where they are available cannot go unnoticed. There might come some routing numbers in the future or the ones readily available revise some of their policies, but as of now, we can make do with the ones we have.

FAQs

Can I transfer money to an IBAN number?

Yes, to transfer money with IBN, you should first ensure you have the correct code. The length of the IBAN code will solely depend on the country where the bank account was opened; some might be longer, while others might have slightly fewer numbers. Here are some lengths of IBAN codes per country.

for France-27 characters

for Poland-28 characters

for Belgium-16 characters

for Norway-15 characters

for Austria-20 characters